- US Dollar Index heads lower again

- Market full of expectations as Joe Biden becomes the 46th US President later today

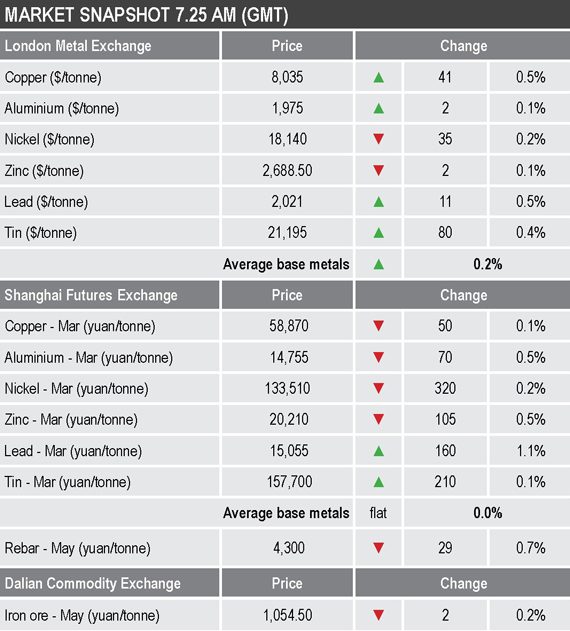

Base metals

Three-month base metals prices on the LME were mixed this morning, with nickel ($18,140 per tonne) and zinc ($2,566.50 per tonne) down by 0.2% and 0.1% respectively, while the rest of the complex was up by an average of 0.4%, led by 0.5% gains in copper ($8,035 per tonne) and lead ($2,021 per tonne).

The most-traded base metals contracts on the SHFE were also mixed this morning, with the March contracts for lead and tin up by 1.1% and 0.1% respectively, while the rest of the metals’ March contracts were down by an average of 0.3%. March copper was down by 0.1% at 58,870 yuan ($9,079) per tonne.

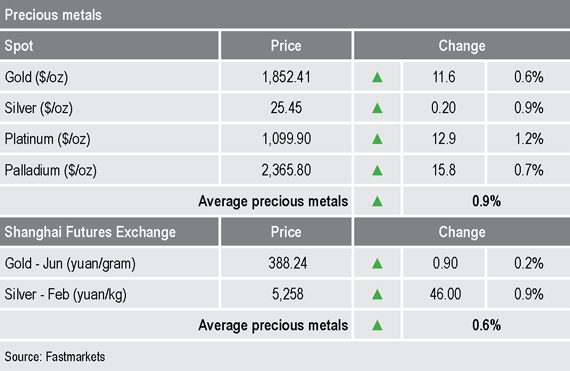

Precious metals

Spot gold was up by 0.6% at $1,852.41 per oz this morning, while silver ($25.45 per oz), platinum ($1,099.90 per oz) and palladium ($2,365.80 per oz) were up an average of 0.9%.

Wider markets

The yield on US 10-year treasuries has found support around the 1.10% level, where it was this morning, unchanged from a similar time on Tuesday.

Asian-Pacific equities were mainly positive this morning: the Kospi (+0.71), the ASX 200 (+0.41%), the Hang Seng (+0.78%) and the CSI (+0.7%), while the Nikkei (-0.38%) was weaker.

Currencies

The US Dollar Index turned lower on Tuesday and was weaker again this morning; it was recently quoted at 90.28, this after 90.75 at a similar time on Tuesday and a recent high of 90.96. The recent low was at 89.21 on January 6.

The other major currencies were mainly firmer this morning in light of the dollar weakness: the euro (1.2153), the Australian dollar (0.7738), sterling (1.3665) and the yen (103.72).

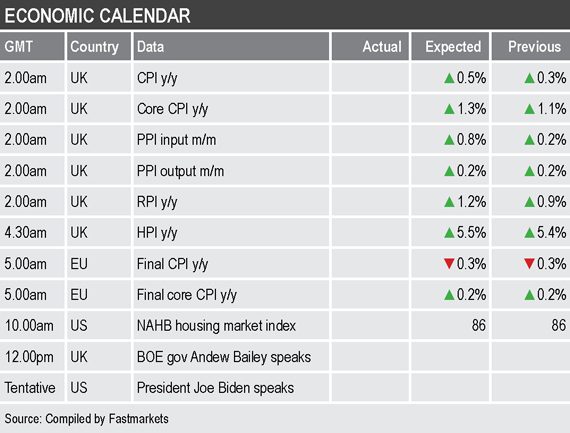

Key data

Wednesday’s economic data includes a barrage of UK price data – see table below – as well as EU consumer prices (CPI) and the US housing market index from the National Association of Home Builders (NAHB).

In addition, Bank of England Governor Andrew Bailey is scheduled to speak, as will Biden at his presidential inauguration.

Today’s key themes and views

We have been saying recently that it will be interesting to see the depth and durability of any pullback in the base metals to gauge how strong underlying sentiment is. Both zinc and aluminium recently set off lower but they already seem to have run into support, this after a 7.9% dip in zinc and a 7.2% dip in aluminium. So for now underlying sentiment does seem robust and the complex’s overall uptrend just pausing/consolidating, rather than stalling.

Gold prices appear to have found support in the middle of their sideways-to-lower trading range, with the weaker dollar probably providing enough support for now. Overall, we see the yellow metal continuing to consolidate its September 2018 – August 2020 bull run that saw prices rise by 78% to $2,074 per oz, from $1,160 per oz. The current range from the down channel runs between $1,716 and $1,886 per oz, so there is considerable room for volatility. We wait to see if the extra spend from Biden’s administration makes investors feel in greater, or less, need of a haven.