- Along with a stronger US Dollar Index, US 10-year treasuries yields are stronger too…

- …suggesting risk-on, but broader markets not reflecting that this morning

- Asian-Pacific equities were weaker this morning

Base metals

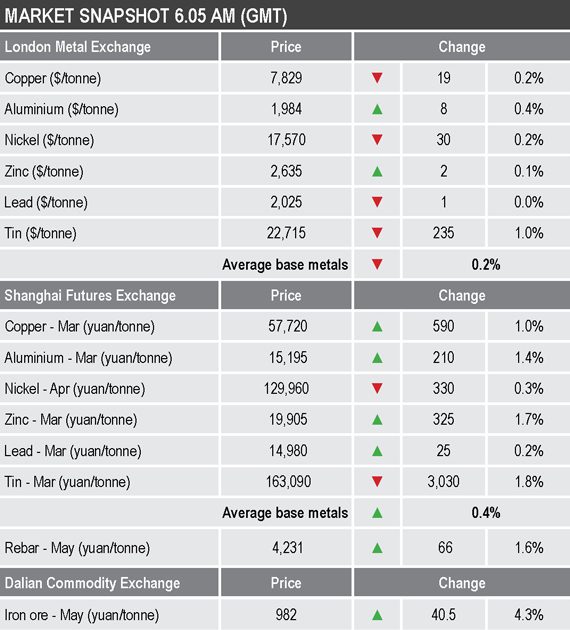

Three-month base metals prices on the LME were mixed this morning, with tin correcting lower and down 1% at $22,715 per tonne while prices pull back from multi-year highs, copper ($7,829 per tonne) and nickel ($17,570 per tonne) both down by 0.2% and lead off slightly at $2,025 per tonne. Zinc ($2,635 per tonne) was little changed and aluminium was up by 0.4% at $1,984 per tonne.

The most-traded base metals contracts on the SHFE were for the most part stronger, the exceptions were April nickel that was down by 0.3% and March tin that was down by 1.8%. March lead was up slightly with a 0.2% gain, while the rest were up strongly with March zinc up by 1.7%, March aluminium up by 1.4% and March copper up by 1% at 57,720 yuan ($8,934) per tonne.

Precious metals

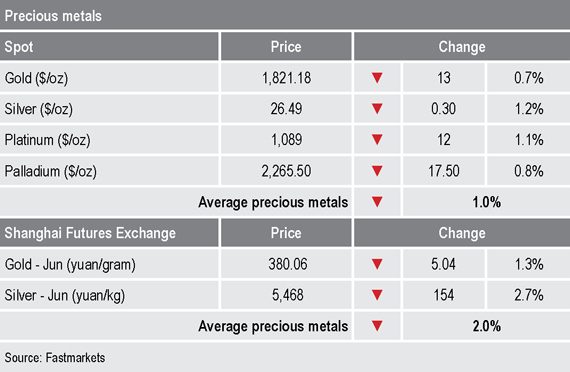

Precious metals were down across the board by an average of 1%, with spot silver ($26.49 per oz) and platinum ($1,089 per oz) down by 1.2% and 1.1% respectively, while spot gold ($1,821.18 per oz) and spot palladium $2,265.50 per oz) were down by 0.7% and 0.8% respectively.

Wider markets

The yield on US 10-year treasuries has extended higher, it was recently quoted at 1.14% this morning, up from 1.11% at a similar time on Wednesday, suggesting a slight pick-up in risk appetite.

But Asian-Pacific equities were weaker this morning: the Hang Seng (-0.9%), the CSI (-0.08%), the Kospi (-1.35%), the ASX 200 (-0.87%) and the Nikkei (-1.06%).

Currencies

The US Dollar Index was edging higher and was recently quoted at 91.29, having in recent days breached previous highs between 90.97 and 91.06. This suggests the dollar could see its countertrend move higher for a while.

Most of the other major currencies were weaker: sterling (1.3607), the euro (1.2013) and the yen (105.18), while the Australian dollar (0.7632) was consolidating above recent lows, probably helped by a 4.3% rebound in iron ore prices on the Dalian Commodity Exchange this morning.

Key data

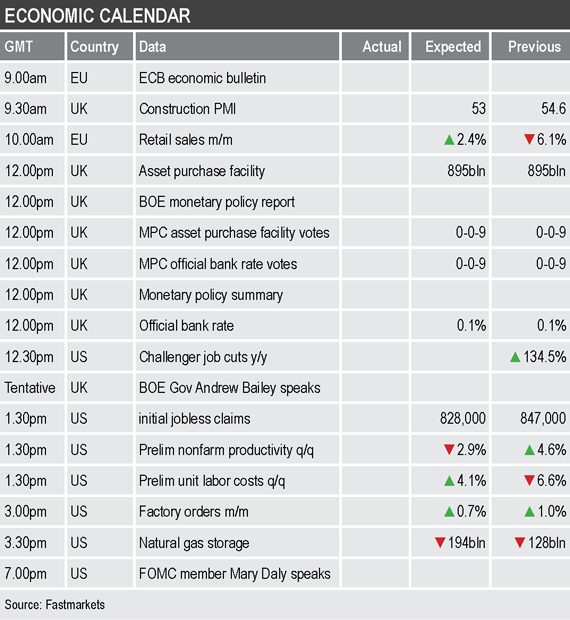

Thursday’s economic agenda is busy, starting with an economic bulletin from the European Central Bank, which is followed by UK construction purchasing managers’ index (PMI) data, EU retail sales, the Bank of England’s interest rate decision and monetary policy update, with Governor Andrew Bailey scheduled to speak too.

US data includes Challenger job cuts, initial jobless claims, preliminary nonfarm productivity and unit labor costs, factory orders and natural gas storage.

In addition, US Federal Open Market Committee member Mary Daly is scheduled to speak.

Today’s key themes and views

While the market’s focus is on the tin backwardation, the metals’ prices are for the most part either extending their pullbacks, or consolidating. The question is, is this just a reaction to the stronger dollar, or the sign of tiredness setting in after some long drawn out rallies that have run since last March?

We see plenty of room for a countertrend move and the current setup should tell us whether there is any appetite to reduce exposure to the metals, or whether the market is just pausing while it gets used to these price levels, before ratcheting higher again once governments’ infrastructure spending starts to reach the order books.

The stronger dollar seems to be pushing the precious metals down to the lower levels of their recent trading ranges, with silver unwinding most of its recent sharp gains.