- India reported 315,000 new Covid-19 infections on Wednesday

- Haven assets on the rise

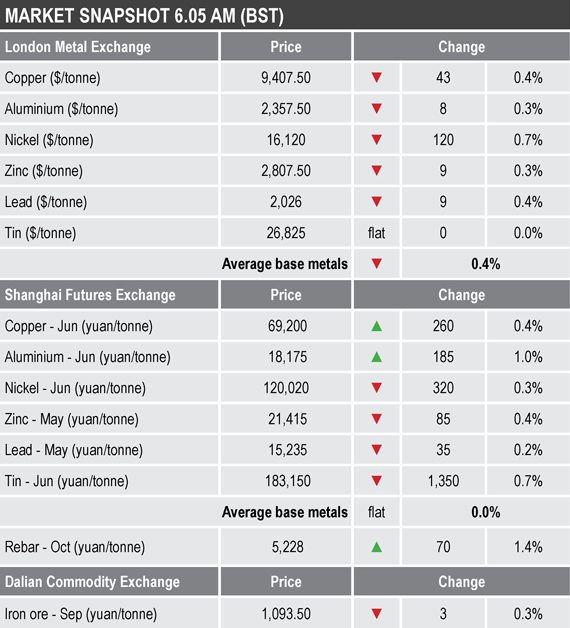

Base metals

LME three-month base metals prices were down across the board by an average of 0.4% this morning, but volume has been low with just 2,681 lots traded as of 6.05am London time. This compares with an average across Monday to Wednesday closer to 4,400 lots at a similar time of day. Nickel ($16,120 per tonne) led on the downside with a 0.7% decline, while aluminium ($2,357.50 per tonne) and zinc ($2,807.50 per tonne) were down the least with 0.3% falls. Copper was off by 0.4% at $9,407.50 per tonne.

The most-active base metals contracts on the Shanghai Futures Exchange were mixed, with the June copper and aluminium contracts up by 0.4% and 1% respectively, with copper at 69,200 yuan ($10,652) per tonne, while the rest of the base metals were down by an average of 0.4%.

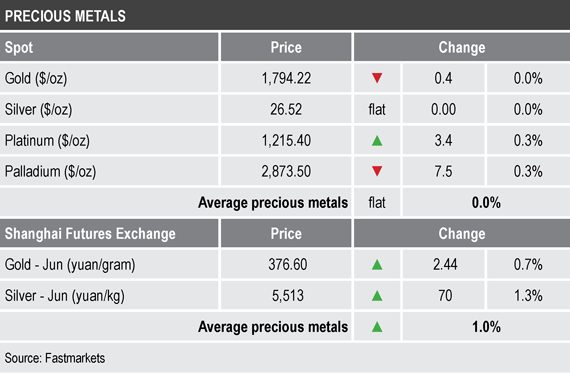

Precious metals

Spot gold ($1,794.22 per oz) and silver ($26.52 per oz) were little changed this morning compared with Wednesday’s closes, but they were up from where they were at a similar time on Wednesday, when they were at $1,783.12 and $25.92 respectively. Platinum ($1,215.40 per oz) was up by 0.3% and palladium (2,873.50 per oz) was down by 0.3%.

Wider markets

The yield on US 10-year treasuries has slipped again this morning and was recently quoted at 1.53%, this after 1.56% at a similar time on Wednesday.

Asian-Pacific equities were mainly stronger on Thursday: the Hang Seng (+0.44%), the Kospi (+0.16%), the ASX 200 (+0.67%) and the Nikkei (+2.12%), while the CSI 300 (-0.23%) was lower.

Currencies

The US Dollar Index was consolidating in low ground this morning and was recently quoted at 91.11, for now holding above Tuesday’s low of 90.85.

The other major currencies were also consolidating this morning: the euro (1.2034), the Australian dollar (0.7744), sterling (1.3934) and the yen (108.05).

Key data

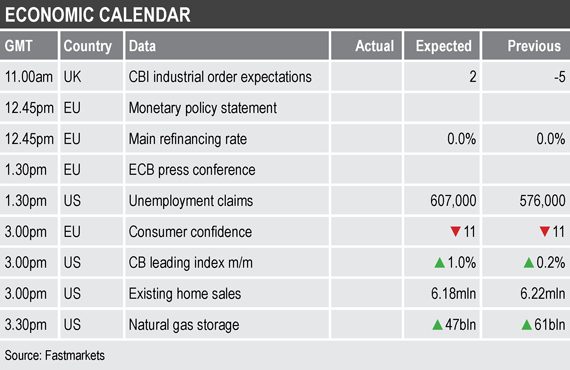

Thursday’s economic data includes industrial order expectations from the Confederation of British Industry, EU consumer confidence and US data on initial jobless claims, leading indicators, and existing home sales.

In addition, the European Central Bank will issue its monetary policy statement, set its main refinancing rate and hold a press conference.

Today’s key themes and views

So far only aluminium has been able to push the envelope on the upside, copper and tin tried to as well but overhead selling dominated, while zinc and nickel remain entrenched in sideways channels and lead’s rebound ran out of momentum mid-range.

With the major Wall Street indices also challenging recent highs again, after only brief pauses earlier in the week, it does look like the markets are in risk-on mode again and the metals may well take their direction from Wall Street. We are, however, wary that gold, the yen and bond yields suggest a pick-up in haven demand, which ties in with our medium-term view that we feel a broad market correction is overdue.

Gold prices are on the rise again after a brief pause on Monday, the weaker dollar and bond yields no doubt providing support, but we would not be surprised if the rise in gold reflects some investors positioning themselves in case a broader market correction unfolds.