The dollar index, at 96.49 as at 9.33am Shanghai time, continues to retreat from the peak of 97.70 reached on November 12.

Providing the base metals with further support were reports that a lack of investment in capacity expansion projects due to the heightened trade tensions between the United States and China since March has contributed to significant falls in base metals’ supply growth rates.

“A lack of investment in new capacity is seeing growth in supply fall. Most base metals have seen the growth rates in supply fall sharply, with some contracting amid the uncertainty,” ANZ Research said on Friday.

Zinc outperformed its peers this morning, with the metal’s most-traded January contract on the SHFE rising to 21,245 yuan ($3,064) per tonne as at 9.33am Shanghai time, up by 220 yuan per tonne from Thursday’s close.

Zinc continues to benefit from a positive fundamental picture; zinc stocks at SHFE-listed warehouses stood at 39,675 tonnes on November 16, down by 53% year on and year and down 49% since the beginning of 2018.

While China’s refined zinc production totaled 4.65 million tonnes in January-October, down 3.1% year on year, according to the latest data from China’s National Bureau of Statistics.

In addition, the International Lead & Zinc Study Group (ILZSG) pegged the refined zinc market in a 54,700-tonne deficit in September and a 305,000-tonne deficit in January-September.

The global refined zinc market is expected to record a deficit of 322,000 tonnes in 2018, up from the 263,000-tonne forecast made in May, and the year 2019 is likely to see a deficit of 72,000 tonnes, according to ILZSG.

“[Zinc] availability is likely to remain tight over the short-to-medium term while utilization rates at Chinese smelters are set to remain low. We therefore believe price risks remain skewed to the upside in the short term because tightness is likely to intensify,” Fastmarkets research analyst James Moore said.

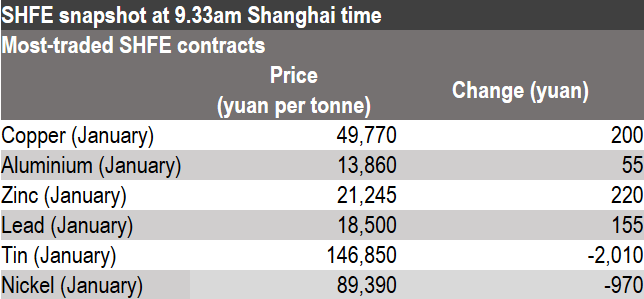

In tin, prices weakened amid concerns of slow demand and rising inventories. The metal’s most-traded January contract price fell to 146,850 yuan per tonne as at 9.33am Shanghai time, down by 2,010 yuan per tonne from Thursday’s close.

“The latest annual survey from the International Tin Association suggests demand growth has been much slower in 2018 compared with the 4% growth recorded in 2017,” according to Moore.

An increase in SHFE tin stocks last week has added fuels to these fears; SHFE tin stocks were up 161 tonnes to 8,188 tonnes in the week to November 16 – up by 27.8% from 6,406 tonnes on September 28. Stocks are up 53.8% in the year to date.

Base metals prices

- The SHFE January copper contract price climbed by 200 yuan per tonne to 49,770 yuan per tonne.

- The SHFE January aluminium contract price moved up by 55 yuan per tonne to 13,860 yuan per tonne.

- The SHFE January zinc contract price rose by 220 yuan per tonne to 21,245 yuan per tonne.

- The SHFE January lead contract price increased by 155 yuan per tonne to 18,500 yuan per tonne.

- The SHFE January tin contract price declined by 2,010 yuan per tonne to 146,850 yuan per tonne.

- The SHFE January nickel contract price fell by 970 yuan per tonne to 89,390 yuan per tonne.

Currency moves and data releases

- The dollar index edged down by 0.02% to 96.49 as at 9.33am Shanghai time.

- In equities, the Shanghai Composite was down by 1.01% to 2,618.78 as at 10.10am Shanghai time.

- The economic agenda was light on Thursday due to US markets being closed for the country’s Thanksgiving Day holiday. Japan’s consumer price index (CPI) for October was recorded at 1.4%, meeting the previous expectations while higher than 1.2% in September.

- Meanwhile, the Eurozone preliminary consumer confidence index for November sit at -3.9, much lower than the expected -3 and the previous -2.7.

- In data today, we have services and manufacturing purchasing managers’ index (PMI) data out across France, Germany, the Eurozone and the US.