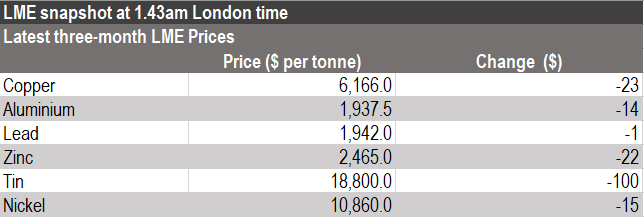

Lead and nickel prices recorded gains – albeit marginal ones – while the rest of the complex weakened, led by a 2% fall in zinc prices.

The dollar index has moved back above 97, recently at 97.06 as at 9.43am Shanghai time, but still remains well below the peak of 97.70 reached on November 12. Nonetheless, the firmer US currency continues to exert downward pressure on base metals prices.

In addition, the intense risk-averse sentiment prevalent among investors, who have held back from trading while they await further direction on the US-China trade war ahead of the upcoming Group of Twenty (G20) summit in Argentina at the end of the week, continues to add to the base metals’ woes.

“Investors continue to monitor the situation around the US-China trade conflict, with the upcoming G20 summit likely to see President Trump and President Xi sit down and discuss a deal,” ANZ Research said on Tuesday.

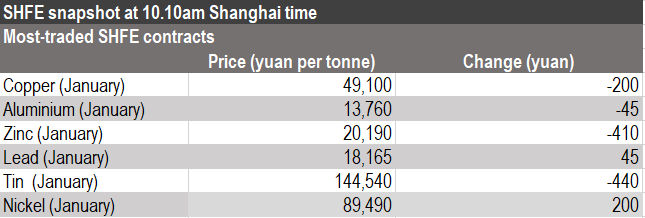

As was the case on Monday, zinc was the worst performer of the SHFE base metals this morning, with metal’s most-traded January contract falling to 20,190 yuan ($2,908) per tonne as at 10.10am Shanghai time, down by 410 yuan per tonne or 2% from Monday’s close.

“The current [zinc] price was mainly dragged down by concerns over the weakening domestic consumer demand as a result of the growingly stringent environmental protection measure in winter for the purpose of air quality improvement,” Citic Futures Research said.

Meanwhile, concerns over increased supply in the market are helping to push zinc prices lower.

“Key global mine restarts and ramp-ups have increased the prospect of rising global mine output, threatening the bull run off the 2016 low,” Fastmarkets research analyst Andy Farida said.

“The ongoing US-China trade war, a rapid slowdown in Chinese economic growth and the strong recovery in the dollar index after its 2018 low in February is also preventing [zinc] from rebounding,” he added.

Lead was little changed with a slight upward bias this morning, no doubt benefitting from signs of tightness in the market.

Lead’s most-traded January contract rose to 18,165 yuan per tonne as at 10.10am Shanghai time, up by 45 yuan per tonne or 0.3% from Monday’s close.

Despite a 450-tonne increase in SHFE lead stocks to 9,295 tonnes last week, inventories remain down by 77.7% in the year to date.

Elsewhere, the global refined lead market was in a deficit of 110,000 tonnes in the first nine months of 2018, according to the International Lead and Zinc Study Group (ILZSG).

Although the size of the deficit is smaller than that of 166,000 tonnes a year ago, the study group pegged the 2018 deficit at 123,000 tonnes, up from previous forecast of 17,000 tonnes.

At the same time, demand is expected to pick up for battery stockpiling season for the winter, providing some support to the metal’s price, according to Farida.

Base metals prices

- The SHFE January copper contract price dropped by 200 yuan per tonne to 49,100 yuan per tonne.

- The SHFE January aluminium contract price went down by 45 yuan per tonne to 13,760 yuan per tonne.

- The SHFE January zinc contract price fell by 410 yuan per tonne to 20,190 yuan per tonne.

- The SHFE January lead contract price edged up by 45 yuan per tonne to 18,165 yuan per tonne.

- The SHFE January tin contract price declined by 440 yuan per tonne to 144,540 yuan per tonne.

- The SHFE January nickel contract price rose by 200 yuan per tonne to 89,490 yuan per tonne.

Currency moves and data releases

- The dollar index went up by 0.02% to 97.06 as at 9.43am Shanghai time.

- In equities, the Shanghai Composite was up by 0.42% to 2,586.68 as at 10.24am Shanghai time.

- In data on Monday, Japan’s manufacturing purchasing managers’ index (PMI) for November was recorded at 51.8, below the previous reading of 52.9.

- Meanwhile, Germany’s IFO business climate reading for the November period was lower than expected at 102, down from 102.8 for October.

- Releases scheduled for Tuesday include the Bank of Japan’s core consumer price index reading, the United Kingdom’s CBI realized sales and US data that includes the monthly house price index, the Standard&Poor/Case-Shiller Composite-20 house price index and Conference Board consumer confidence.

- In addition, US Federal Open Market Committee members Richard Clarida and Raphael Bostic are speaking.