- China’s CSI 300 up by 2.6%; LME base metals up an average of 0.4%, after a 1.2% gain on Tuesday

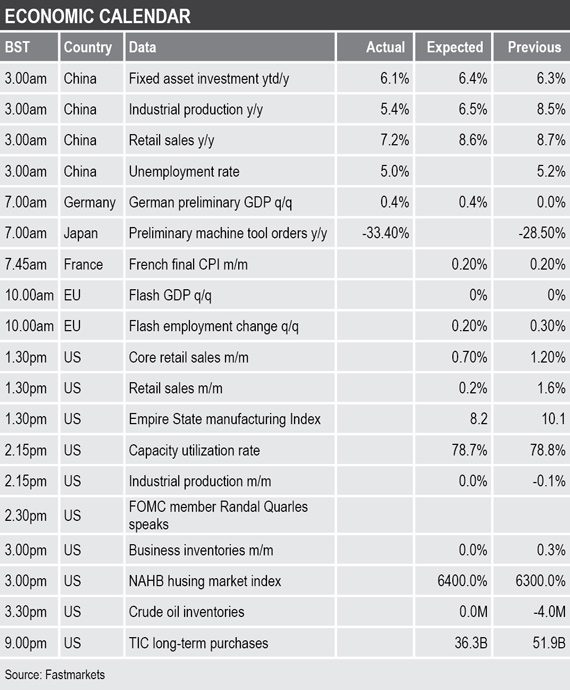

- China’s fixed asset investment, industrial production and retail sales, all come in below forecast

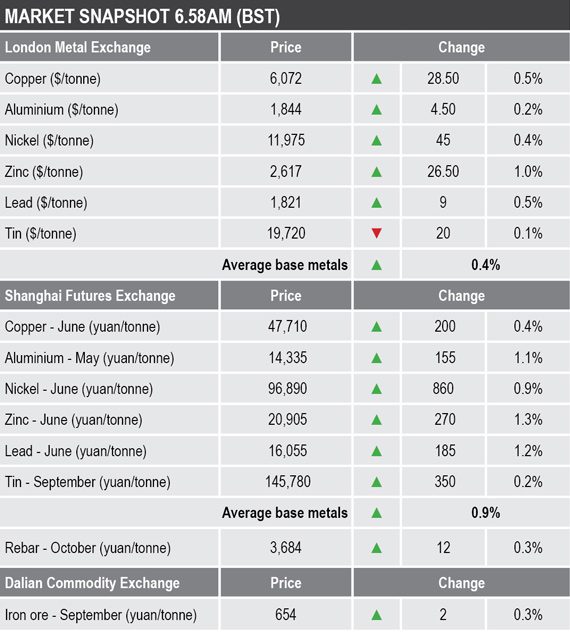

Base metals

The London Metal Exchange base metals complex was for the most part firmer on Wednesday, the exception was tin that was down by 0.1%, but that comes after a 1.9% rally on Tuesday. Zinc led on the upside with a 1% gain, and copper was up by 0.5% at $6,072 per tonne, compared with a low of $6,007.50 per tonne on Monday.

Following weakness on Monday, a strong performance was seen on Tuesday with the complex closing with average gains of 1.2%. Aluminium was up by 1.6%, nickel rose by 1.4% and lead ended the day with a gain of 1.2%. Zinc and copper were the laggards with increases of 0.5% and 0.4% respectively.

One reason for the rebound seems to be a counter reaction to the trade related sell-off on Monday with the market thinking they may have been initially too negative about the trade situation after US President Donald Trump’s comments on Tuesday that talks with China will be “very successful”.

Hopes were also running high that weak Chinese economic data will mean the country’s government boosts stimulus, which is fueling the equity rebound too.

In China, base metals prices on the Shanghai Futures Exchange were up across the board on Wednesday, with prices up by an average of 0.9% – led by gains averaging 1.2% in the June zinc, lead and aluminium contracts. The June copper contract was up 0.4% at 47,710 yuan ($6,936) per tonne, compared with 47,490 yuan per tonne at Tuesday’s close.

Spot copper prices in Changjiang were down by 0.2% at 47,450-47,650 yuan per tonne and the LME/Shanghai copper arbitrage ratio was slightly weaker at 7.86, compared with 7.87 at a similar time on Tuesday.

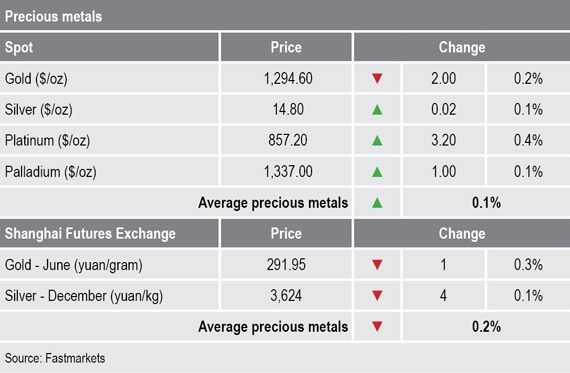

Precious metals

Spot gold prices were slightly weaker at $1,294.60 per oz on Wednesday morning, this compared with Tuesday’s high of $1,303.65 per oz. The more industrial precious metals are up by an average of 0.2%.

On the SHFE, the June gold contract was down by 0.3% from Tuesday’s close, while the December silver contract was off by 0.1%.

Wider markets

In wider markets, the spot Brent crude oil price was little changed at $70.94 per barrel, compared with $70.95 per barrel at Tuesday’s close.

The yield on benchmark US 10-year treasuries was firmer at 2.4130%, compared with 2.4095% at a similar time on Tuesday. The yields on the US two-year and five-year treasuries returned to being inverted having all but flattened out on Tuesday and were recently quoted at 2.2088% and 2.1956% respectively.

The German 10-year bund yield has moved further into negative territory, it was recently quoted at -0.0792%, compared with -0.0705% at a similar time on Tuesday.

Asian equity markets were unsurprisingly down this morning: Nikkei (-0.59%), Hang Seng (-1.7%), CSI 300 (-0.32%), the Kospi (-0.11%) and the ASX 200 (-0.92%). The fact that Asian equities were not down by more, considering the sell-off in the United States on Monday, suggests some stability is returning.

This follows a stronger performance in western markets on Tuesday. In the US, the Dow Jones Industrial Average closed up by 0.82% at 25,532.05, while in Europe the Euro Stoxx 50 was up by 1.31% at 3,364.38.

Currencies

The rebound in broad market sentiment has given the US dollar some support with the dollar index recently quoted at 97.54, this after a low on Monday of 97.03.

The firmer dollar is weighing on the other major currencies: the euro (1.1203), sterling (1.2904), the Australian dollar (0.6923) and the Japanese yen (109.57).

The yuan’s spell of weakness seems to have paused with it recently quoted at 6.8673, this after it had fallen to a low on Tuesday at 6.8865, from around 6.7100 in mid-April. The other emerging market currencies are mixed.

Key data

Data out already on Wednesday showed broad weakness in China with fixed asset investment falling to 6.15, from 6.3%, industrial production falling to 5.4%, from 8.5% and retail sales falling to 7.2%, from 8.7% – all showing considerable deterioration. But China’s unemployment rate did fall to 5% from 5.2%.

The first reading of German gross domestic product (GDP), for the first quarter, climbed by 0.4%, having been flat in the fourth quarter last year.

Other key data out today includes France’s consumer price index, EU GDP and employment change, with US data that includes retail sales, Empire State Manufacturing Index, industrial production, capacity utilization, crude oil inventories and Treasury International Capital (TIC) data. In addition, US Federal Open Market Committee member Randal Quarles is speaking.

Today’s key themes and views

With rebounds underway we will now have to see if there is follow-through buying interest. Given the weak Chinese economic data and the uncertainty over the US-China trade talks, with no resolution likely until we get closer to the Group of Twenty (G20) summit on June 28-29, we expect trading to remain choppy.

While we would not rule out further price weakness, the market could be setting itself up for a strong reversal, especially as the funds are believed to be significantly short and the fundamentals for all the metals remaining tight, with Fastmarkets expecting deficits to remain in place in all the base metals this year.

Gold found some support last week on the back of the turmoil in trade talks and that was built upon on Monday with prices breaching $1,300 per oz. With broader markets now rebounding, gold may well start to struggle again.