- A Democratic-controlled Congress could, however, cause some headwind for some sectors of the equity markets, although those involved in the rollout of electrification could do well

- US 10-year treasury yields have moved back above 1%

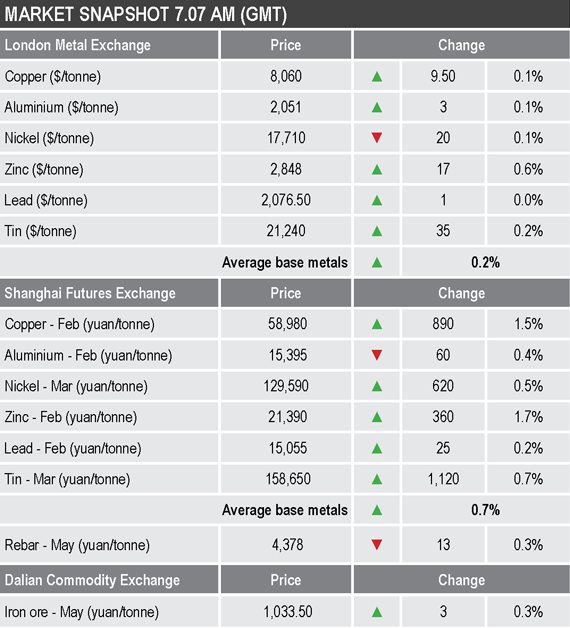

Base metals

Three-month base metals prices on the London Metal Exchange were mainly slightly firmer this morning, the exception was nickel that was off by 0.1% at $17,710 per tonne, but the underlying trends across the board remain upward. The rest of the metals were up by an average of 0.2%, skewed by a 0.6% rise in zinc ($2,076.50 per tonne), while copper was up by 0.1% at $8,060 per tonne – the highest it has been since February 2013.

Most of the most-traded base metals contracts on the Shanghai Futures Exchange were stronger this morning; the exception was February aluminium that was down by 0.4%, while the rest were up by an average of 0.9% – led by a 1.7% rise in February zinc. February copper was up by 1.5% at 58,980 yuan ($9,130) per tonne.

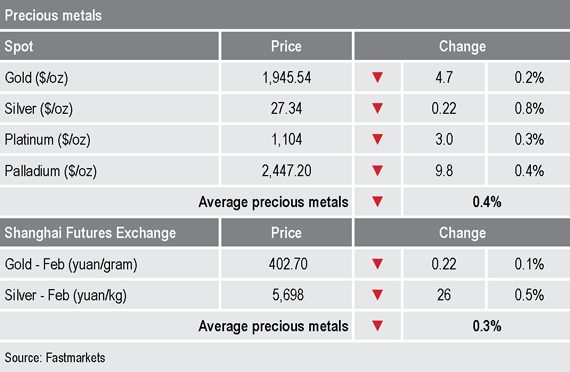

Precious metals

All the precious metals were weaker this morning, with the complex down by an average of 0.4%, with spot gold down by 0.2% at $1,945.54 per oz. Given the likelihood of a Democratic-led Congress, which could be seen as an inflationary, it is surprising gold prices were weaker this morning, especially given the weaker dollar, but that said, they have done a lot on the upside already in recent days.

Wider markets

As already mentioned above, the yield on US 10-year treasuries has moved back above 1% and was recently quoted at 1.02%, compared with 0.92% at a similar time on Tuesday.

Asia Pacific equities were mixed this morning: the CSI (+0.92%), the Hang Seng (+0.29%), the ASX 200 (-1.12%), the Nikkei (-0.38%) and the Kospi (-0.75%),

Currencies

In line with the expected Democratic -win theme above, the US dollar index has extended its decline and was recently quoted at 89.24, the lowest it has been since March 2018.

Given the dollar weakness, the other major currencies were stronger this morning: the euro (1.2339), the Australian dollar (0.7796), sterling (1.3652) and the yen (102.74).

Key data

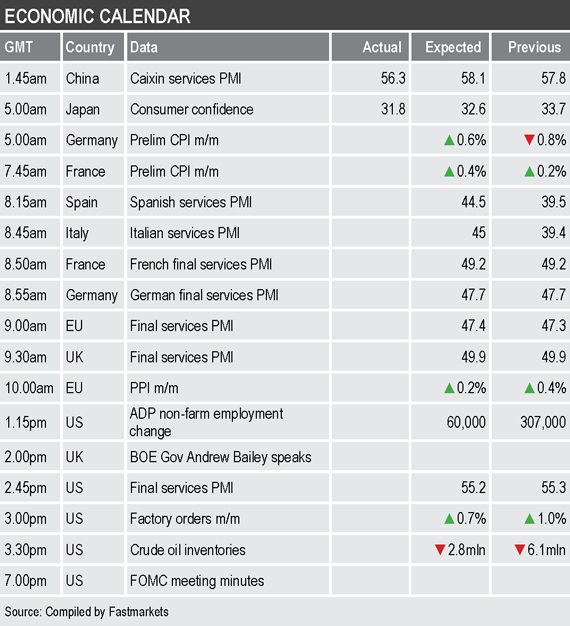

Today’s economic agenda is extremely busy with the focus on services purchasing managers’ index (PMI) data, which is out across all regions, with China’s Caixin reading dropping to 56.3 in December from 57.8 in November.

There is also data on Japanese consumer confidence, French and German consumer price indices (CPI) European producer price indices (PPI) as well as US releases that include ADP non-farm employment change, factory orders and crude oil inventory.

In addition, Bank of England governor Andrew Bailey is scheduled to speak and the Federal Open Market Committee (FOMC) will release the minutes of its latest meeting.

Today’s key themes and views

With copper and tin pushing the envelope on the upside, it now looks more than likely that the other base metals will continue to rebound off the end-of-year corrections and push into open water too. As such, it looks like the weight of money, the inflation-hedge attributes that commodities have and the macro underlying story (infrastructure spending) are all fueling the rally. While we feel the current and medium-term fundamentals do not justify such strength, we would not stand in its way.

Gold’s acceleration to the upside on Monday and follow-though strength since, suggests another up-leg is underway and if the Democrats take hold of the US Senate then the inflationary outlook might increase and that could fuel gold’s rally further.