It is hard to find bright sparks in the months ahead for the ferrous supply chain, which has been buffeted repeatedly in a short span of few months, starting with Chinese Premier Li Keqiang’s comments on overheated commodity markets and promises of stronger action on “questionable market practices” in July.

Iron ore crash

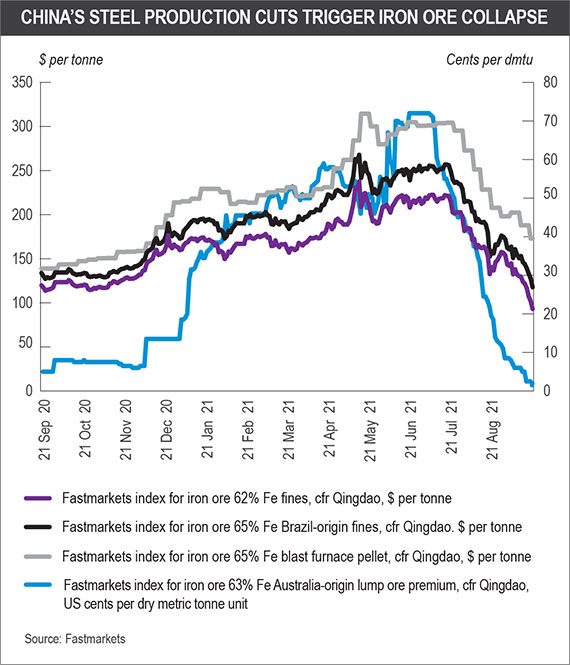

The Chinese government’s move of extending pollution controls and steel production caps across China is causing iron ore to flirt dangerously with the $80-per-tonne prices last seen in March 2020 not long after Covid-19 first broke out.

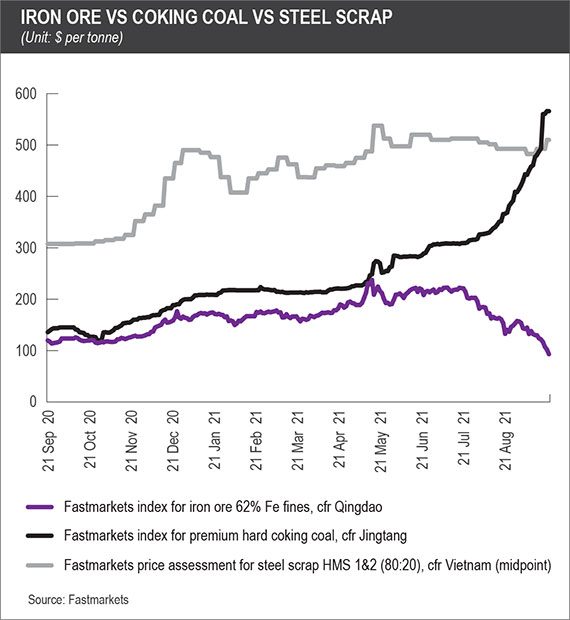

This has reduced the value of iron ore to just a fraction of that for coking coal and ferrous scrap – complementary steelmaking raw materials in blast furnaces and electric-arc furnaces.

Iron ore prices have fallen to just 1/6 of those for coking coal and 1/5 of those for scrap.

How long can the bearish sentiment remain in the iron ore market?

There are plenty of tell-tale signs.

Market sources expect iron ore supply to continue to head to Asia, with major miners looking to increase their production and shipping guidance.

BHP expects to produce 246-255 million tonnes of iron ore in its 2022 financial year, focusing on “incremental volume growth through productivity improvements,” it said in its annual report. It also expects its share of the Samarco pellet project to produce 3-4 million tonnes of the steelmaking raw material.

It increased its total iron ore production by 2% to 252 million tonnes in the 2021 financial year ended June 30 after ramping up production at South Flank, Jimblebar and Mining Area C.

Vale reported a 16-million-tonne increase in iron ore production in the first half of its 2021 financial year, with the output for fines rising by 11.3% to 75.7 million tonnes in the same period.

This was attributed to higher volumes from its Brucutu operations, better weather conditions in Serra Norte, and higher productivity at its Itaira complex, it said in a production report in July. Its Serra Leste iron ore mine also achieved full capacity.

Vale’s iron ore production guidance for 2021 remains at 315-335 million tonnes, and market sources are not expecting any reduction despite the rapidly falling demand from the Chinese market.

Data from the China Iron & Steel Association showed that the country’s iron ore imports fell by 1.7% in January-August period to 746.45 million tonnes.

In Asia, iron ore cargoes are already being diverted, with major steelmakers looking to reduce their term-contract commitments and channel shipments to other buyers in the region, sources told Fastmarkets.

The impact of this on spot prices is telling.

Fastmarkets’ iron ore 62% Fe fines, cfr Qingdao hit year-to-date low of $92.98 per tonne on September 20; this is down 61% from an intra-year high of $237.57 per tonne on May 12.

Fastmarkets’ iron ore 65% Fe fines, cfr Qingdao fell to a year-to-date low of $117.60 per tonne on September 20; this is 56% lower than an intra-year high of $267.80 per tonne on May 12.

Fastmarkets’ 63% Fe Australia-origin lump ore premium was at 1.50 cents per dry metric tonne unit on September 20 – its lowest so far this year. It is down by 98% from an intra-year high of 72 cents per dmtu on June 18.

Fastmarkets’ iron ore 65% Fe blast furnace pellet, cfr Qingdao hit a year-to-date low of $173 per tonne on September 17; this is 45% lower than an intra-year high of $314.50 per tonne on May 14.

Evergrande and Communism 2.0

China’s second-largest property developer Evergrande’s financial woes are also weighing on markets.

On top of dampening steel demand in China, there is a risk of its default extending far beyond construction and into financial markets, as well as increased governmental scrutiny on major Chinese companies.

A collapse of Evergrande and its effects on China’s building and construction sector could cause damage by reducing rebar demand in September-October, typically the year’s second peak season, sources said.

“The rebar import market is quiet because buyers are looking to see whether the Evergrande situation worsens,” a South Asian rebar trader told Fastmarkets on Friday September 17.

This could also mean a sharp loss in demand for imported billet in China.

“If that happens, billet prices could come down very sharply,” the same trader told Fastmarkets.

China has been a key supporter of the global steel billet and scrap markets, with its mammoth appetite soaking up millions of tonnes to feed its domestic re-rolling capacity amid recurrent blast furnace cuts.

Fastmarkets’ price assessment for steel billet, import, cfr China has remained largely stable this year. The assessment was at $710-720 per tonne on September 17, down by $60-80 per tonne (8-10%) from $770-800 per tonne seen on May 14.

But a Chinese mill source said the ongoing steel production cuts would continue to be a big factor supporting prices and driving demand for imported billet.

Market participants have described the current situation as a fast-spreading “market contagion,” especially with other listed A-Shares on the Shanghai Stock Exchange also taking a beating.

It adds to the increased governmental scrutiny of other major Chinese companies such as Tencent and Didi Chuxing even as China clamps down on major companies and restructures them for reasons such as data protection and fair competition.

The attempt by the Chinese government to redistribute wealth for “common prosperity,” which is especially targeted at the upper echelons of Chinese society such as technology billionaires, has been described by the international audience as “Cultural Revolution 2.0” or “Communism 2.0.”

This has caused uneasiness in the financial markets, of which steel futures form a part of.

Adding to this is the expected quantitative easing by major central banks around the world – the United States Federal Reserve is expected to make such a move in 2022 after its fourth-quarter meetings.

All in all, the global ferrous complex looks set for a rough six months ahead until after the Chinese New Year and the Winter Olympics in Beijing in early February.

(The 19th paragraph should have read as “intra-year high of 72 cents per dmtu on June 18” instead of “intra-year high of $72 per tonne on June 18” as originally published. This has been corrected.)