By Jocelyn Garcia, price reporter, agriculture

In recent weeks the corn export pace has slowed markedly, with net sales data recording a string of consecutive marketing year lows ahead of the data release on Thursday August 5.

“There are lots of uncertainties running around now,” Larry Shonkwiler of Advance Trading told AgriCensus, citing surprisingly low-key US export sales to destinations other than China, despite major rival exporters like Brazil and Argentina facing major crop and logistics issues.

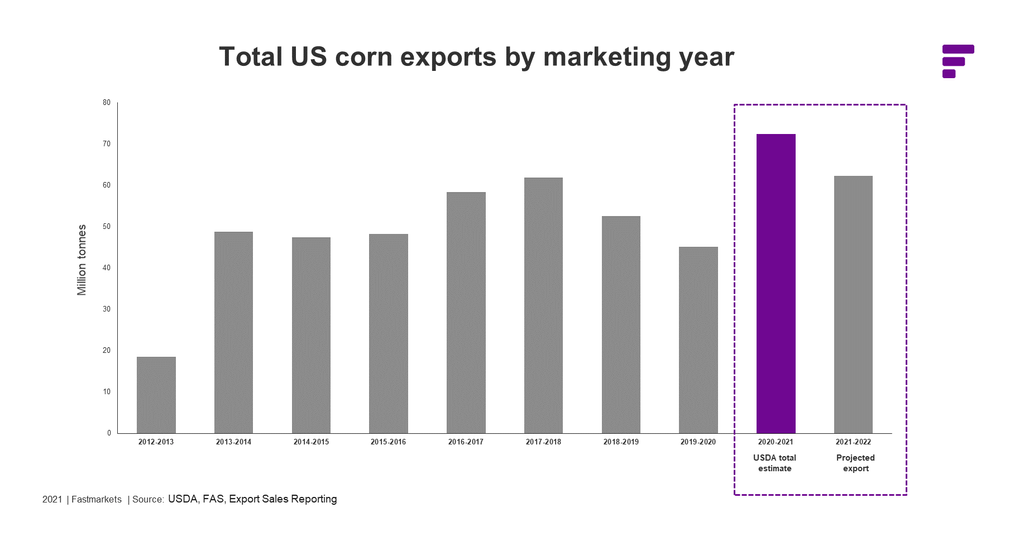

Weekly US export sales in the week to Friday July 29 placed accumulated exports for the current marketing year at 63,522,800 tonnes.

Even if the current pace of 1 million tonnes per week were to continue to the end of the marketing year, or if the outstanding sales of 6,200,700 tonnes were to be realized, the total figure is unlikely to hit the USDA estimate of 72,390,000 tonnes.

This translates to an estimated 3 million tonnes of corn that is currently forecast to be exported making its way back into 2020-2021 ending stocks, while outlooks for the upcoming 2021-2022 production continue to hover around a record-breaking 385 million tonnes.

Last week, US net sales for corn revealed a net sales reduction of 88,500 tonnes, further solidifying the unlikelihood that the 2020-2021 marketing year will reach USDA predictions, but will become a new record figure, nonetheless.

And the US faces its own logistics issues, with the main Asia-facing Pacific Northwest hub struggling to secure enough supply into its ports after farmers across the Plains were forced to claim prevent-planting insurance after bad weather stopped planting.

It is worth noting that despite exports seeming to move at a slower than expected pace, compared to the same point last year, accumulated exports are still up 64%.

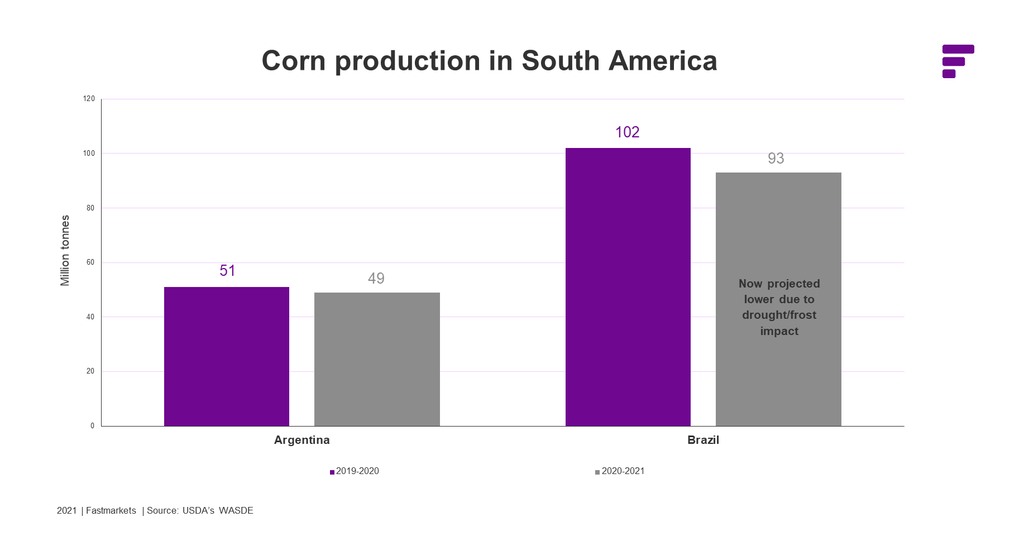

Argentina and Brazil, the main competing origins to Asian markets, are both experiencing decreased production and thus decreased export potential, meaning that demand is likely to shift to US corn.

As of yet, this does not appear to be the case, posing the question of why US exports may be experiencing a slowdown?

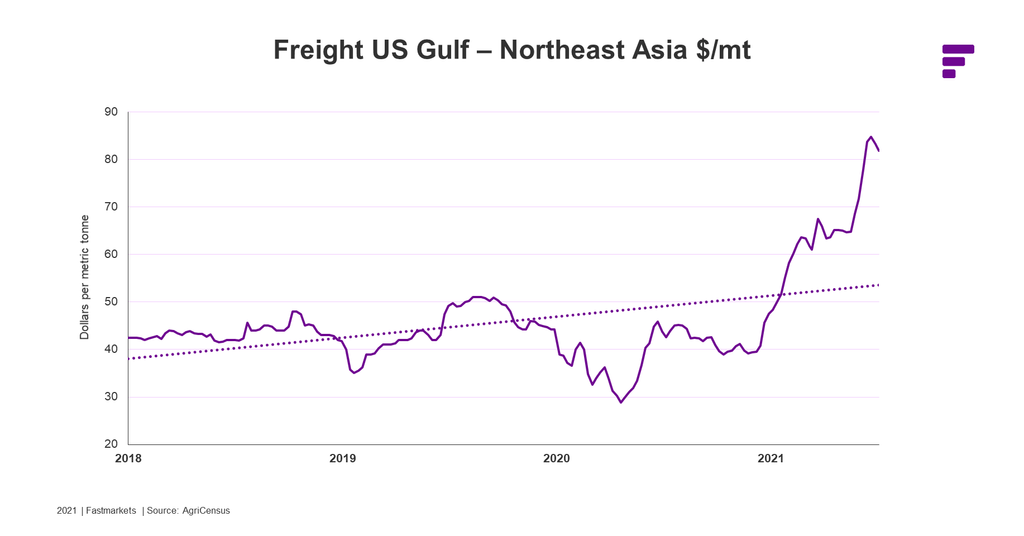

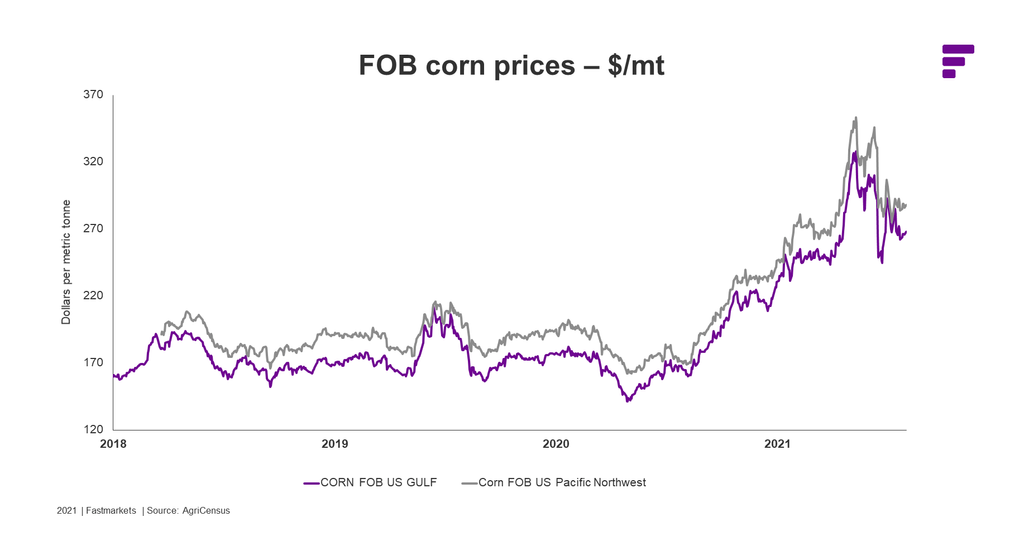

This year’s unprecedented levels seen for both corn and freight costs are factors in the hand-to-mouth buying being observed.

As Shonkwiler points out, “some argue buyers are simply waiting for cheaper corn prices since the US is pretty decent, as well as for ocean freight to come off its lofty level”.

Data from the latest USDA weekly crop progress report revealed a drop in corn conditions week-over-week that came at the bottom of the range of analysts’ estimates, adding to overall uncertainty about the state of the market.

Another factor at play is the uncertainty surrounding China.

“There are questions about the recent flooding in China and whether that will increase demand for imports, or reduce feed use if animal numbers were significantly impacted,” Shonkwiler said.

Furthermore, African swine fever (ASF) is still a factor impacting feed demand in the country with the country’s Ministry of Agriculture and Rural Affairs confirming 11 outbreaks of ASF this year in last month’s news briefing.

The USDA’s current estimated production output for China for this marketing year would reflect a slight decline compared to the 2019-2020 marketing year, but an increase of 3% is projected for the upcoming marketing year.

Has China’s corn demand decreased?

As another trade source put it, “is it more of a function of China just holding steady on the side lines. It appears it’s just a culmination of all these events, which are contributing to the general feeling of malaise on exports”.

Market movement is expected to pick up once the new crop comes in.

A third market contact offered this perspective: “Importers will seek alternative sources as they wait for the US crop to develop, but eventually they must come to the US”.

Senior Commodity Analyst at Futures International, Terry Reilly, backed this sentiment.

He said: “We look for old crop corn commitments to remain low but new-crop sales to increase in coming weeks.”

This article, by Jocelyn Garcia, was first published to agricensus.com on August 5.