While there were mixed messages about demand in certain downstream sectors, such as superalloys (mostly applied in the aerospace sector), a strong performance in the electric vehicle (EV) sector, alongside a cautious expectation of steady or growing demand in the key consumer electronics sector, means that the overall outlook for 2021 is a rapid uptick compared with 2020.

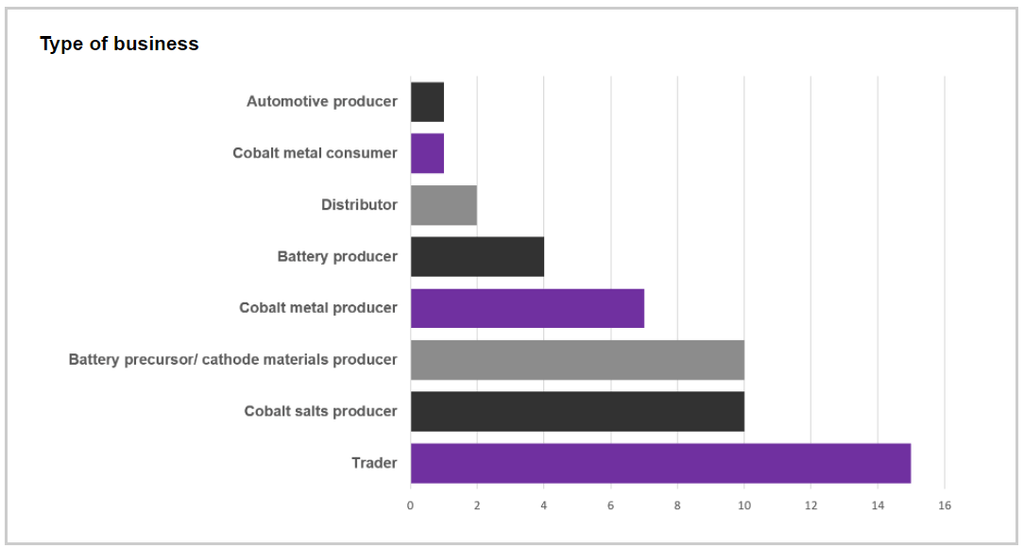

In our survey, Fastmarkets received effective responses from a total of 50 market participants, comprising 15 traders, 10 cobalt salts producers, 10 battery precursor/cathode materials producers, seven cobalt metal producers and four battery producers. The remaining responses came from two distributors, a cobalt metal consumer and an automotive producer. Where participants were active in more than one market, they were listed under their main business category.

The survey responses show clear a positive tone toward the cobalt demand outlook, with most participants eyeing steady or stronger demand for cobalt in 2021, compared with 2020, when the wide-scale disruption caused by the Covid-19 pandemic has a detrimental impact on all industrial activities.

In total, looking at six key sectors, survey respondents gave 143 positive answers in terms of demand expectations for 2021 with just 24 negative responses.

Cobalt demand is expected to rise 17% in 2021 from 2020 when downstream appetites return – especially in the industrial sectors – which were largely subdued due to the pandemic, according to William Adams, the head of Fastmarkets’ battery raw materials research team.

“Demand in 2021 will be elevated given the dip in 2020,” Adams said.

EV sector to drive stronger demand

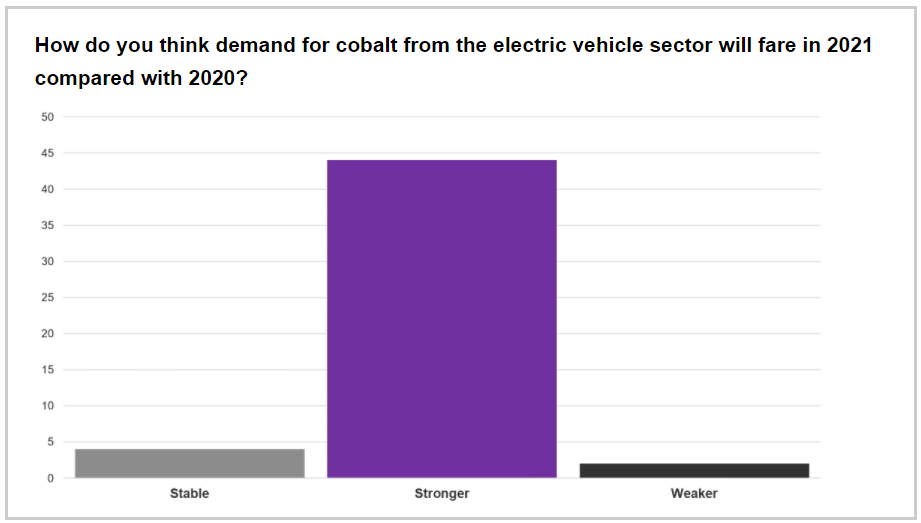

An overwhelming 44 respondents expect demand for cobalt from the EV sector to grow in 2021, with only two anticipating a reduction.

The pandemic slowed the production and sales of EVs due to the suspension of manufacturing activities in the first and second quarters of 2020, although Original Equipment Manufacturers (OEMs) tried to play catch-up in the second half of the year, encouraged by financial incentives and changes to local regulations related to sustainable industries.

And fast-changing public opinion about investing in more environmentally friendly forms of transport will further boost sales of EVs in 2021, market participants told Fastmarkets.

Even considering the impact of the coronavirus, global pure EV (PEV) sales are expected to have grown by 32% in 2020, and sales will rise by 43% year on year in 2021, according to Adams.

But the growth of cobalt demand from nickel-cobalt-manganese (NCM) lithium-ion EV battery manufacturers is being challenged by a resurgence in interest among China’s OEMs in lithium iron phosphate (LFP) batteries.

LFPs generally have a lower energy density than NCMs, resulting in shorter driving ranges in EVs, but their revival is likely to continue through 2021 due to the recent rapid rallies in cobalt and nickel prices.

Fastmarkets’ price assessment for cobalt sulfate 20.5% Co basis, exw China rose to 64,000-66,000 yuan per tonne ($9,874-10,182) on Friday January 15, up by 20.4% from 53,500-54,500 yuan per tonne on December 9, 2020, when the price began to gradually tick upward.

And Fastmarkets’ price assessment for nickel sulfate min 21%, max 22.5%; cobalt 10ppm max, exw China stood at 31,500-32,000 yuan per tonne on January 15, up by 16.5% from 27,000-27,500 yuan per tonne on November 20, 2020, when the price started to rise.

That said, the increasing adoption of EVs globally – particularly in Europe – and OEMs in China making a slower transition to NCM 811 (Ni:Co:Mn: 8:1:1) lithium-ion batteries from NCM 523 and NCM 622 should boost demand for cobalt in 2021, according to market participants.

For the past five years or so, the majority of OEMs in China have focused on developing nickel-rich batteries, namely the NCM 811, which provides the highest driving range among existing NCM batteries and therefore garnered attractive government subsidies. But this usage of nickel-rich batteries has slowed as a result of a technical bottleneck in the form of cost and safety issues and a reduction in EV-related subsidies.

“OEMs prioritize safety more than anything else and there are still some technical uncertainties with nickel-rich batteries regarding the performance in stability and safety,” a battery cathode materials producer said. “As such, OEMs are likely to slow their ambitions in developing nickel-rich batteries in the near term.”

A second battery cathode materials producer said that because the pandemic is still causing lockdowns in Europe and elsewhere around the world, the commercialization of EV models that use nickel-rich batteries has been delayed.

“While greater deployment of LFP batteries has ‘stolen’ some market share from NCMs, we expect the strong growth in demand for EVs in Europe and in China, to fuel demand for NCM and nickel-cobalt-aluminium (NCA) batteries,” Adams said.

“Whereas a few years ago we would have expected NCM 811 to be one of the main batteries in use by now, we think the deployment of NCM 811 has been slower than expected, with more OEMs content with NCM 532 and NCM 622, which will have a positive impact on cobalt,” he added.

Consumption of consumer electronics has developed much more strongly than many people had initially expected in 2020, largely due to the surge in demand for work-from-home (WFH) equipment, which mainly relates to traditional personal computers (PCs), laptops and peripheral equipment.

Global shipments of PCs grew 13.1% year on year in 2020, according to the International Data Corp (IDC).

But some market participants remain skeptical about whether this momentum will be maintained in 2021, citing some of the demand that was due to emerge this year might have been brought forward into 2020 after businesses and educational establishments were forced to equip their staff (and pupils) to work remotely because of the pandemic.

“Unlike smartphones, it takes a longer period of time for consumers to replace their old laptops,” the second battery cathode materials producer said.

“With lithium cobalt oxide (LCO) batteries going into consumer electronics, such as laptops and tablets, the market did well in 2020 because there was a rush to get people equipped to work from home. But that might mean there is relatively less demand in 2021, unless smartphones on the fifth-generation (5G) network fill in the gap,” Adams said.

It is estimated that 5G smartphone shipments will reach close to 19% of the global volume of mobile phones in 2020 and grow to 58% in 2024, according to IDC.

“Since smartphone sales were subdued last year due to economic headwinds amid the pandemic, consumer appetites to change devices due in 2020 might [have been] delayed until 2021,” a battery producer said. “That will add to cobalt demand and offset the potential decline in consumption of PCs.”

Mobile phone sales in China, the largest consumer of the globe of this category, fell by 20.8% year on year in 2020, according to the China Academy of Information and Communications Technology (CAICT).

Mixed opinions on demand outlook from superalloys

After a significant drop in aerospace activity in 2020, when the Covid-19 pandemic limited international air travel, market participants are generally optimistic about a recovery in cobalt demand from the superalloys sector, though some negative aspects were too significant to be downplayed, the survey results show.

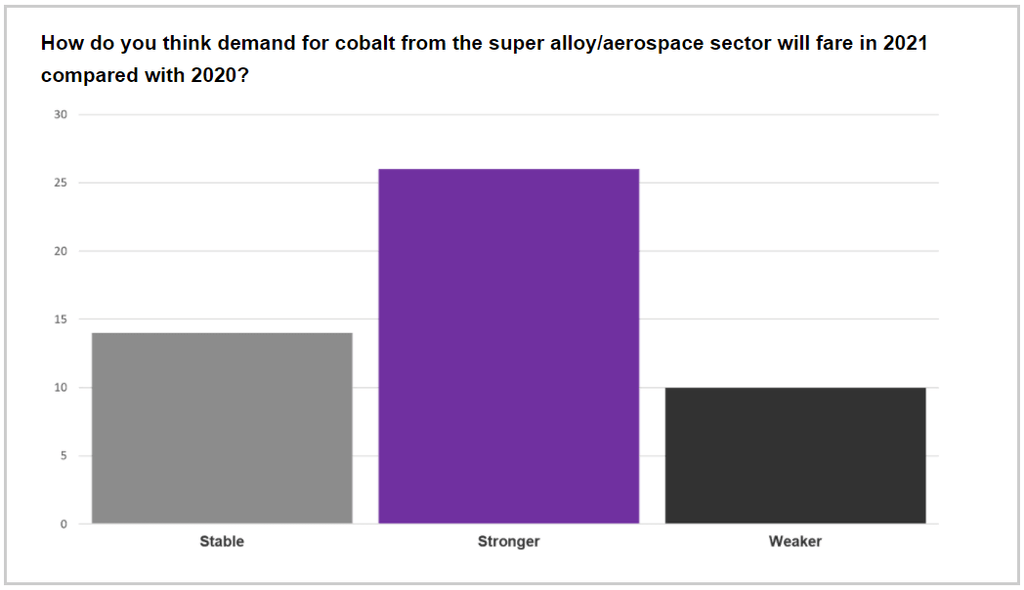

Cobalt demand from the superalloys sector will grow stronger in 2021 compared with 2020, according to 26 survey respondents, while 14 expected demand to be unchanged. But the survey of this sector also had the largest negative responses among the six – the remaining 10 respondents were bearish – showing that market participants’ opinions are not all that aligned on how the sector will fare in the coming 12 months.

Sellers with exposure to this market have conflicting outlooks – some reported having supplied stable volumes to those buyers last year, while others have said there had been no interest from superalloys producers in negotiating contracted volumes for 2021 given the overhang of material.

Aerospace was one of the highest-profile casualties from the pandemic after Covid-19 saw international travel shrink and carrier fleets grounded.

But market participants holding positive views pointed out despite airliners canceling orders, the two main aircraft producers – Boeing and Airbus – both had backlogs of several thousand planes all waiting to be produced.

In addition, the global rollout of Covi-19 vaccines will be a boon for the sector, although several market sources said they did not anticipate that this would filter through to an increase in passenger travel until at least the second half of 2021.

Other industrial sectors steady

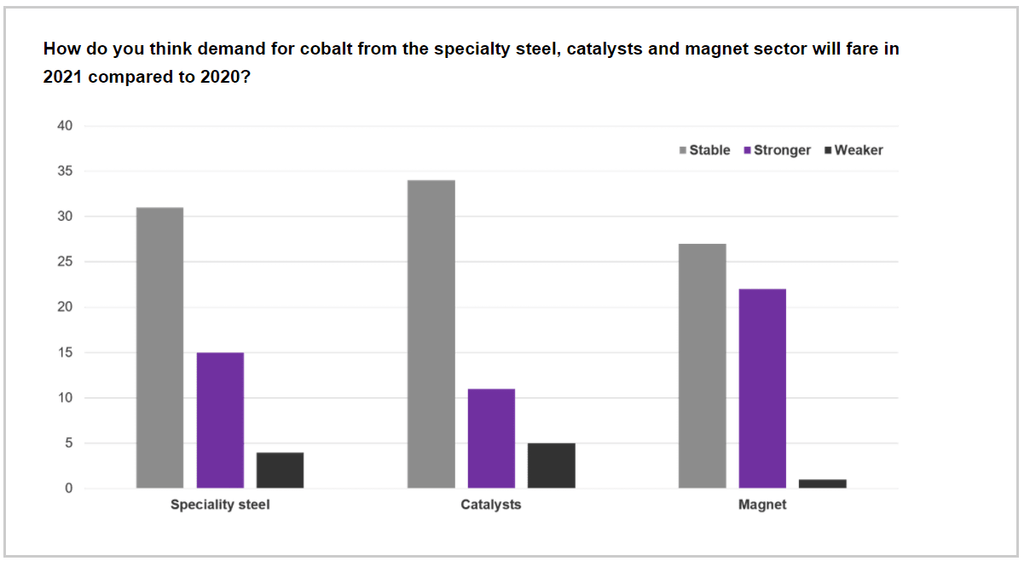

For other industrial downstream sectors, such as specialty steel, catalyst and magnet manufacturers, the consensus among survey respondents suggests that they would at least generate stable demand in 2021 compared with 2020. However, quite a few market participants were anticipating stronger demand, especially from the magnet sector.

Similar to superalloys, market participants said the rollout of vaccines would boost the recovery of other industrial sectors where cobalt is used. However, the scale of that recovery will depend on how fast the vaccines reach the furthest flung reaches of the planet.

“I would have thought more [of those who responded to the survey] would have seen demand stronger as the rollout of vaccines is likely to see confidence return to the industrial sectors as the year progresses,” Adams said.

Elsewhere in cobalt’s downstream sectors, the catalyst market fared well in 2020 – only experiencing a downtrend in demand for two or three months, according to one catalyst producer.

“For 2021, the catalyst market is very healthy. The more stringent regulations around [emissions] is positive, as it requires more catalysts to be used per the amount of fuel,” the source said.

Adding that the market was currently growing faster than global gross domestic product (GDP) and the demand for catalyst in the internal combustion engine (ICE) vehicle market are yet to be affected by the pick-up in vehicle electrification.

While this is a positive for the cobalt market, the catalyst sector is, ultimately, quite small compared with the volumes other markets require – sitting at around 1,000-1,500 tonnes annually, according to the source.

The magnet sector, too, is a niche part of the market, but because it takes much smaller volumes than either aerospace or EVs, it is therefore less affected by swings in demand.

“Demand looks fair to strong, with what appeared to be a return of some demand in the second half of last year. Whether that is tied to magnets primarily used in the automotive sector – where demand suddenly reappeared late last year – I am not sure, but the sector looks steady,” a trader said.

A second trader pointed out that magnets are required in industrial gas turbines, an area that was seeing good demand.

Overall, despite a turbulent 2020, market insiders have a positive outlook for the cobalt market in 2021.

Keep up with the trends and news from the cobalt market, visit our dedicated cobalt market analysis page.